Since 1989, most central banks around the world have adopted an inflation targeting regime. This column argues that credit for how much inflation targeting (IT) contributed to the pre-2021 decades of low inflation has run ahead of the evidence. Forces such as globalisation and simple ‘regression to the mean’ should be taken seriously, alongside inflation targeting adoption, as explanations for low inflation between 1989 and 2021. Going forward, inflation targeting must evolve to survive and maintain credibility in the face of shocks such as financial crises and supply disruptions.

In Bhalla et al. (2023), we carry out a comprehensive examination of the performance of inflation targeting across advanced and emerging market economies since 1989. Our overall assessment of the regime is favourable but hedged: we argue that, while inflation targeting has worked well in the face of myriad challenges, credit for how much inflation targeting contributed to the pre-2021 decades of low inflation has run ahead of the evidence.

Inflation targeting started out with a bang. All nine of the initial adopters of the regime saw a decline in the three-year average inflation following adoption.

This successful initial policy offering was followed by two ‘quick wins’ as a couple of initial fears about the regime proved to be unfounded. The first fear had been that emerging markets lacked the human and intellectual capital to adopt inflation targeting regimes and that it would thus remain an advanced economy curiosum (e.g. Masson et al. 1997); however, over the past two decades, many emerging markets have successfully adopted the regime, making it a universal standard.

The second fear had been that central banks would become – in the colourful phrase of Mervyn King (1997) – “inflation nutters” (that is, they would elevate achievement of the inflation goal above all others). In practice, central banks have implemented inflation targeting in a flexible manner, giving weight to both output stabilisation and inflation control. For instance, Dąbrowski et al. (2025) study 36 inflation targeting frameworks across advanced economies and EMDEs and find most countries practice flexible inflation targeting.

But, despite the initial success and these two quick wins (universal adoption and flexibility in implementation), our overall assessment of inflation targeting is hedged: we think that credit for how much inflation targeting contributed to low inflation has run ahead of the evidence. In our paper, we provide evidence that:

1. The decline in inflation under IT regimes may simply reflect ‘regression to the mean’. The Ball and Sheridan (2004) critique states that inflation may have gone up for transitory reasons in late 1980s and early 1990s and would likely have come down even in the absence of IT adoption. Inflation targeting is merely a placebo that gets undeserved credit. Ball and Sheridan offer a telling analogy to make their point. Batting slumps – temporary phases where batters have trouble getting hits – are a ubiquitous feature of baseball. Suppose that, during one such slump, a batter is advised by his coach to sleep with his bat next to his pillow. The slump disappears, as slumps do, but the batter incorrectly gives credit to his coach’s advice. Proponents of inflation targeting regress the average change in inflation rate on a dummy variable for IT adoption and show that the coefficient estimate is negative. However, this coefficient becomes insignificant once regression to the mean is controlled for by including the pre-IT inflation rate as an additional explanatory variable.

We illustrate this by comparing the change in inflation rate after adoption of inflation targeting with the initial inflation rate in Figure 2. Countries that experienced a higher inflation rate (shown on the x-axis) happened to have also been the ones which experienced the largest declines in their inflation (y-axis) after the adoption of inflation targeting. We find that Ball and Sheridan’s conclusion still holds, even with a few additional decades of data; moreover, it holds with as much force for EMDEs as for advanced economies. In short, ‘regression to the mean’ remains a powerful explanation for the supposed better inflation performance of IT adopters.

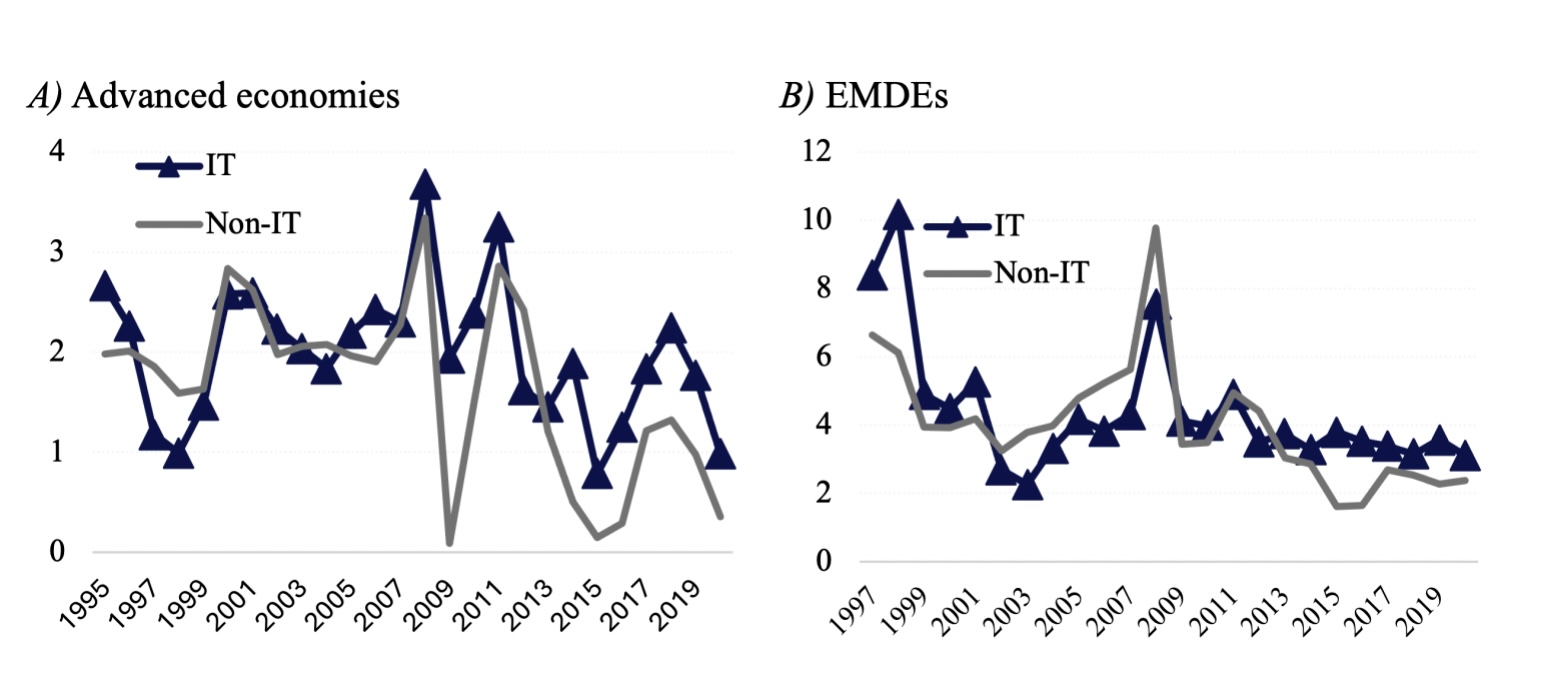

2. Some, such as Rogoff (2003), have argued that alternative factors such as globalisation may be behind the fall in inflation, but credit is often given to inflation target adoption. Prima facie evidence for Rogoff’s point is presented in Figure 3, which shows median inflation across advanced economies and EMDEs for IT and non-IT countries. It is evident that some factors were contributing to a global rise in inflation in the 1990s and since then inflation has moderated across both advanced economies and EMDEs, and this was irrespective of whether the country adopted a formal inflation target regime.

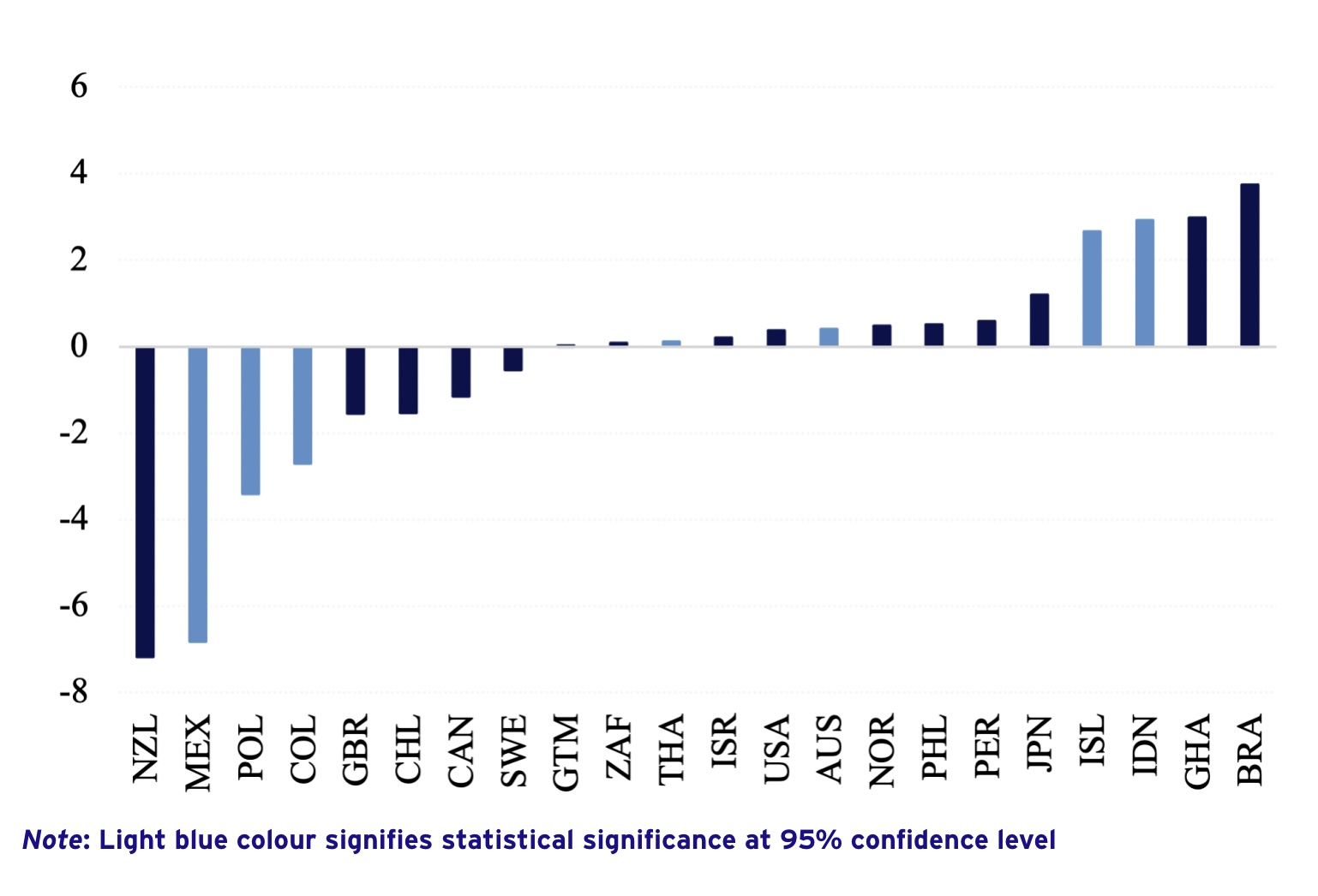

We go further in trying to isolate the contribution of inflation targeting to moderating inflation through a country-by-country synthetic control method (SCM) analysis. That is, we compare the inflation performance in an inflation-target-adopting country with that of a synthetic ‘twin’ country that did not adopt an inflation target regime. The synthetic ‘control’ country shares the key characteristics of the ‘treatment’ country (the inflation target adopter), including similar inflation experience prior to the adoption of an inflation target. The results from our synthetic control analysis suggest that inflation targeting significantly lowered inflation (compared to that in the synthetic control) in only six of our 23 cases. This is shown in light blue in Figure 4.

Despite chinks in its theoretical armour, inflation regimes have performed well in practice partly due to the flexibility of the framework. Faced with numerous shocks such as financial crisis or supply disruptions, central bankers have expanded their policy toolkit to manage often conflicting objectives. A decade after Reichlin and Baldwin (2013) summarised the debate on inflation targeting, we concur that inflation targeting must evolve to survive and maintain its credibility. At the same time, we caution against attributing the great moderation in inflation to the adoption of inflation targeting – alternative explanations such as the effects of globalisation or regression to the mean should be given serious consideration.

Ball, L M and N Sheridan (2004), “Does inflation targeting matter?”, in The inflation targeting debate, pages 249–282, University of Chicago Press.

Bhalla, S, K Bhasin and M P Loungani (2023), “Macro effects of formal adoption of inflation targeting”, International Monetary Fund.

Dąbrowski, M A, J Janus and K Mucha (2025), “Shades of inflation targeting: insights from fractional integration”, Working Paper.

De Grauwe, P (2007), “There is more to central banking than inflation targeting”, VoxEU.org, 14 November.

Frankel, J (2012), “The death of inflation targeting”, VoxEU.org, 19 June.

Ghosh, A R, J D Ostry and M Chamon (2012), “On Inflation Targeting and Forex Intervention: Are Two Targets Better Than One?”, VoxEU.org, 27 May.

King, M (1997), “Changes in UK monetary policy: Rules and discretion in practice”, Journal of Monetary Economics 39(1): 81-97.

Leijonhufvud, A (2007), “The perils of inflation targeting”, VoxEU.org, 25 June.

Masson, M P R, M M A Savastano and M S Sharma (1997), “The scope for inflation targeting in developing countries”, International Monetary Fund.

McKibbin, W J and A J Panton (2018), “Twenty-five Years of Inflation Targeting in Australia: Are there Better Alternatives for the Next Twenty-five Years?”, Conference–2018.

Reichlin, L and R E Baldwin (eds.) (2013), Is Inflation Targeting Dead?: Central Banking After the Crisis, CEPR Press.

Rogoff, K (2003), “Globalization and global disinflation”, Federal Reserve Bank of Kansas City Economic Review 88(4): 45-80.